Johnian magazine issue 55, spring 2026

Beaufort Society: The rise and fall of retirement

Professor Helen McCarthy (2008) is an historian of modern Britain. She shared with Beaufort Society members a talk about the social and cultural history of retirement since 1945. Her book on the subject is set to be published by Penguin.

Turning 80 in 1947, Stanley Jones reluctantly accepted that it was time to throw in his job selling home furnishings in London’s East End. “All I was brought up to was bed to work, work to bed,” he told one of the many social researchers studying the elderly in the early years of the postwar welfare state. While few held on as long as Stanley, earning into old age, those studies revealed, was far from uncommon for working-class people. Men became eligible at 65 for the state pension, but 3 in 5 chose to defer in favour of paid work. At 67, 2 in 5 were still employed. “I’ll retire when someone poleaxes me,” commented Charles Woodman, still in harness as a building labourer in his mid-seventies.

Stanley and Charles were the last Victorians. Born at the end of the 19th century, their adult lives were blown about by two global conflicts and economic crisis in between. For their descendants, retirement would be transformed into something more recognisable to us today: a period of material comfort and well-earned leisure, stretching to 15, 20 or even 30 years. Yet the generation entering the workplace in 2026 might find Stanley and Charles’s experiences a more reliable guide to the future.

Giving up paid work at 60 or 65 is a startlingly recent invention. Long-serving officials in the civil service and a handful of private firms began to receive employer-provided pensions from the 1850s, while the first state pensions were introduced in 1908. These were means-tested and could only be claimed at 70, meaning that earning for as long as physically possible remained, for most, the best defence against poverty in later life. The retirement pensions introduced by Labour after the Second World War were an improvement, but still offered only basic subsistence. With so many other needs to meet, “it is dangerous to be lavish in any way to old age,” warned William Beveridge, key architect of the postwar welfare state.

This was the world in which men like Charles and Stanley clung tightly to their jobs, fearful of losing their living and everything that went with it, from the regular routine of the working day to standing pints for mates down the pub. Yet despite this powerful incentive to keep working, employment rates amongst those of pensionable age fell steeply across the following decades. Nearly a third of men aged 65 or over were still at work in 1951. Thirty years later, the figure was just one in eight. For women, the situation was more complicated: many gave up wage-earning for marriage or motherhood, and those remaining in (or re-entering) paid work became eligible for the state pension at 60. Yet for men and women alike, the trend was towards ever-earlier retirement.

The factors behind this were complex. Greater use of fixed-age retirement by employers pegged to pension schemes enforced exit, while labour market shifts reduced demand for older workers. Some of the ‘lighter’ jobs that had previously been available – feeding machines, sweeping yards, breaking up scrap – fell prey to mechanisation. Meanwhile rising unemployment put pressure on those in declining industries to go early. “When they tell you at the meeting that you should go if you can, it puts you in a bit of a funny position, doesn’t it?” one man recalled. “The management announced the offer to all the over-fifties at a meeting in the canteen … then the union man got up and said it was very generous and would stop redundancies coming in. You can’t really ignore that, can you?”

For some, giving up work was a personal tragedy. Derek Richards deeply resented being pushed out aged 61. “I don’t like to think about how others see me,” he reflected. “Either they must assume I’m older than I am or that I was unable to keep up to my job, which is quite untrue.” Others, by contrast, were happy to claim some leisure, having worked continuously since finishing school at 14. “Apart from the war, I had worked for the same firm for 44 years as a cashier,” explained an early leaver. “I felt due for a rest from presure and I also felt it quite wrong to work until you are too old to enjoy life, which I do.”

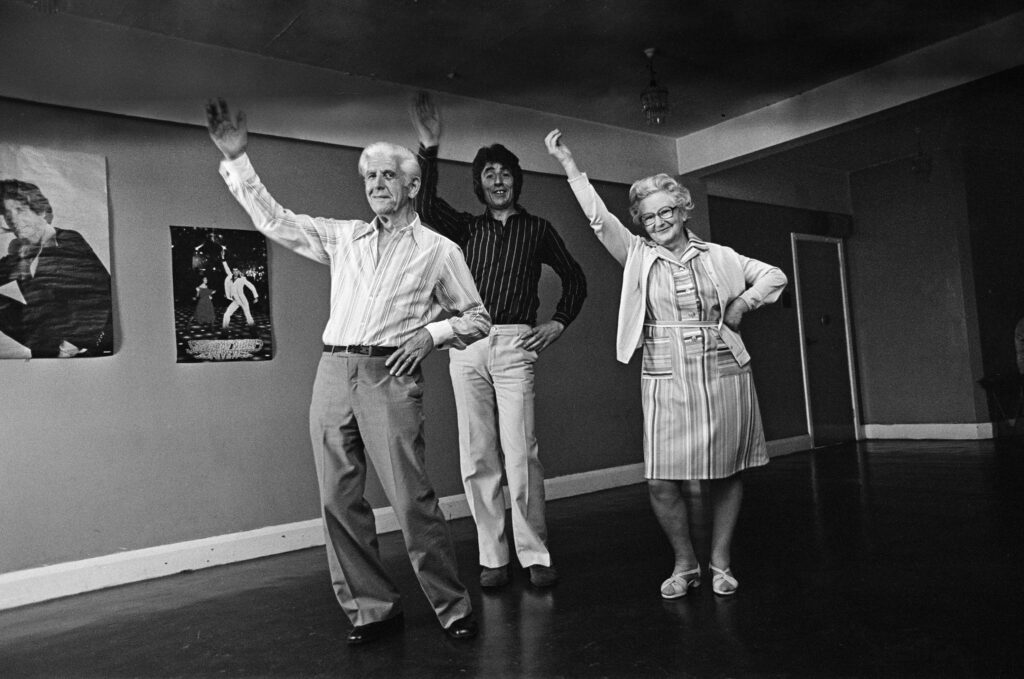

This comment signalled how retirement was changing in the late 20th century. Poverty in old age was still a major risk, but the newly retired were more likely than ever before to have occupational pensions and to own homes. Cheap package holidays, Open University degrees, keep-fit classes and garden centres brought a fresh interest unknown to earlier generations of retirees. This was the era of ‘The Third Age’, a phrase originating in adult education circles but quickly becoming shorthand for all the ways in which advances in health, leisure and material security were transforming the lives of older people. The Baby Boomer cohorts, born after the Second World War, made the Third Age their brand for ageing around the millennium. Better off and healthier than any previous generation of retirees, the Boomers regarded the domestic comforts prized by their parents as indescribably dull. “I certainly don’t want the sort of retirement that my father had,” said a 58-year-old health consultant in the early noughties: “He bought a bungalow on the South Coast and spent his time in the bungalow and pottering around. I wouldn’t do that.” The son instead had his sights set on establishing an architecture practice in Spain, targeting its swelling population of British homeowners, among them many retirees.

Not everything was golden for the over-sixties in the early 21st century. A significant minority still struggled on low incomes, among them divorced women lacking pension rights, migrants with precarious employment histories, and the chronically ill or disabled. The Global Financial Crisis hit many retirees hard, imperilling pension pots, property assets and investments. Yet the bigger story was undoubtedly one of social progress. In 2003 for the first time in postwar history, the proportion of pensioners experiencing relative poverty dropped below the national average. By 2019, pensioner couples were least likely of all household types to be found in the bottom 15 per cent of incomes.

This achievement has prompted remarkably little celebration. Instead, since the 2010s, the growing wealth of the old has fuelled intergenerational tensions, captured in the titles of books such as David Willetts’ The Pinch: How the Baby Boomers Took Their Children’s Future – And Why They Should Give It Back (2010). Younger Britons, Willetts argued, were finding themselves locked out of home ownership in order to preserve Boomer pensions and assets, with no guarantee of a similarly comfortable old age for themselves. Demographics were skewing politics to serve the interests of older voters, as exemplified by Brexit, which younger people overwhelming opposed. “All the policies seem to be aimed at pensioners for the upcoming election,” reflected a 23-year-old woman in early 2024.

These economic and political realities have cast a long shadow over retirement’s future. For most of the 20th century, Britons expected to retire in greater comfort and with more choice than their parents or grandparents. That dream is now at risk, conveyed in the pessimistic outlook of younger cohorts, who watch the pension age rise as they struggle with low wage growth, high housing costs, expensive childcare and inflated food and energy prices.

Historians are cautious about projecting the past into the present. It is entirely possible that gloomy predictions about the burden of population ageing will be proved wrong by technological change, geopolitical events or environmental catastrophe. For the moment, the hardships that stalked the postwar lives of men like Stanley and Charles in the 1950s seem disturbingly prescient.

Living the Dream: The Rise and Fall of Retirement by Helen McCarthy will be published by Penguin (Allen Lane) in 2027-28.